Image by Getty Images

Jacob Harrod, Contributing Member 2020-2021

Intellectual Property and Computer Law Journal

Introduction

A great disparity exists in the American financial markets, and now more than ever the gap between those with power and those without is evident. To be sure, a similar disparity exists throughout the world, in many countries.[1] One need look no further than the contrasting treatment of retail and institutional investors in a company’s initial public offering (IPO) process to see that there is an evident and systemic problem.[2] This Article, however, will focus on the United States stock market, and the relationship that exists between retail investors, institutional investors, and the government.

The dramatic rise and advancement of technology in the 21st century now allows citizens to connect and coordinate information like never before. It also allows a once disparate band of retail investors to gain market knowledge at an unprecedented level and discuss this knowledge amongst themselves over the internet.[3] The speed and efficiency of sharing information over the interest means that investors can form educated assumptions about the potential movement of various securities. Technology in the form of retail trading applications also allows people (who otherwise would not invest) to download an application on their phone, open a brokerage account, and start trading assets and securities, all on the same day.[4] One cannot overstate how profound this shift is, and how it continues to change the shape of the financial markets. As this Article will make clear, the Coronavirus Pandemic has only accelerated this process.

This Article argues that technology and the pronounced rise of the retail investor have highlighted the need for an alteration in the way institutions and the government operate in the market. In particular, the bar for a finding of market abuse and market manipulation should be higher for retail investors than for hedge funds and mutual funds (i.e. institutional investors). Indeed, in certain circumstances, where a hedge fund may be liable for market manipulation, it should not be possible to find a retail investor liable, even when perpetuating the same or similar activity. The government, through securities law, must also do more to curb certain harmful actions that institutions take; such actions are more harmful to the retail investor than ever before.[5] This Article will explain the reasons for shifting relationships in the market, beginning with a brief history of the main players in the United States stock market; what this Article refers to as The Big Three (Institutional Investors, Retail Investors, and the United States Government).

At present, there is also an excellent, ongoing example of the “war” waging between retail and institutional investors, which highlights the somewhat awkward position of the government in terms of moderating the conduct of these groups. GameStop, a seemingly defunct chain of brick-and-mortar video game stores, saw its stock skyrocket, plummet, and dramatically rise again in just the first few months of 2021.[6] One can attribute this unprecedented movement in stock price to the actions of both retail and institutional investors, and the government is still in the process of determining how, when, and why to apply securities laws to the situation. As well as this, the landscape is undergoing a process wherein the current laws are evaluated, and new ones contemplated.[7]

Retail Investing

Put simply, a retail investor is an individual who commits “capital for their personal account rather than on behalf of another company.”[8] Most people probably know someone who invests in the stock market, either on their own through a brokerage account or perhaps through their place of employment. An individual can hold stock directly or can own stock indirectly through mutual and pension funds.[9] Looking at the Federal Reserve’s Balance Sheet of Households and Nonprofit Organizations for Quarter 3 of 2020, retail investors hold approximately 13% of all indirectly held stocks and 23% of directly held stocks.[10]

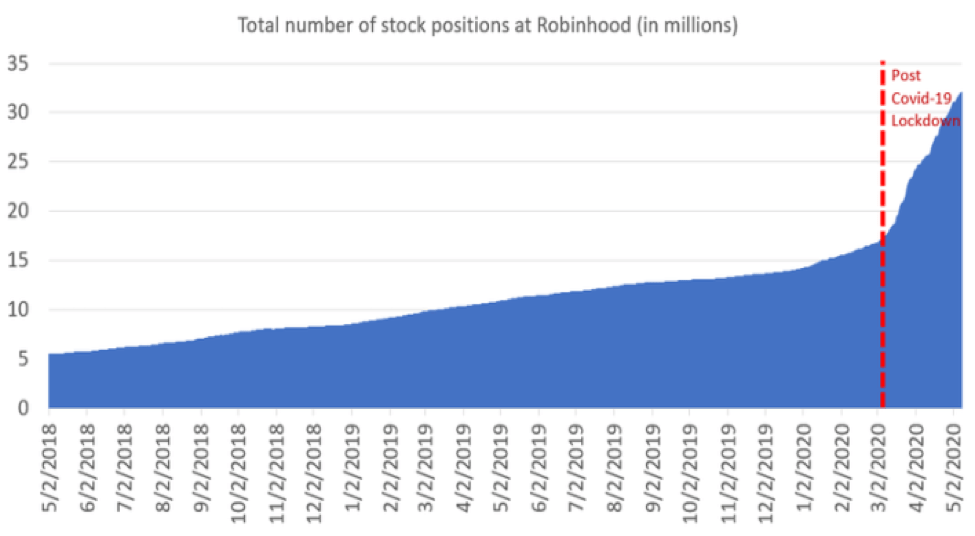

There is no exact figure for exactly how many retail investors exist. However, looking at the usage numbers for some of the most popular trading platforms, the number is clearly in the tens of millions. TD Ameritrade, for instance, provides investment services for over 11 million clients.[11] By the end of 2020, over 13 million people were using the investment application Robinhood.[12] Indeed, Robinhood has more than doubled its client base since 2018.[13] Fidelity has over 30 million brokerage accounts,[14] as does Vanguard.[15] Of course, not all of these accounts are controlled by American citizens. The majority of them are, however, and these are but a few of the many platforms available to retail.[16]

Institutional Investing

An institutional investor is simply an organization that invests money in the market.[17] This group includes mutual funds, investment companies, and pension funds.[18] Namely, and of primary importance to this Article, this group of investors also includes hedge funds.[19] Unlike a mutual fund, which the SEC defines as “a company that brings together money from many people and invests it in stocks, bonds or other assets,”[20] and which are available to the public on normal trading platforms, a hedge fund is private.[21] As the Securities and Exchange Commission (SEC) states:

Hedge funds pool investors’ money and invest the money in an effort to make a positive return. Hedge funds typically have more flexible investment strategies than, for example, mutual funds. Many hedge funds seek to profit in all kinds of markets by using leverage (in other words, borrowing to increase investment exposure as well as risk), short-selling and other speculative investment practices that are not often used by mutual funds.[22]

Whereas a retail investor may take part in a mutual fund on a trading platform, only accredited investors may participate in a hedge fund.[23] The SEC continues:

Typical investors include institutional investors, such as pension funds and insurance companies, and wealthy individuals. Hedge funds are not subject to some of the regulations that are designed to protect investors. Depending on the amount of assets in the hedge funds advised by a manager, some hedge fund managers may not be required to register or to file public reports with the SEC. Hedge funds, however, are subject to the same prohibitions against fraud as are other market participants, and their managers owe a fiduciary duty to the funds that they manage.[24]

Recently, the SEC amended and expanded the definition of “accredited investor” found in Rule 501(a) of Regulation D under the Securities Act of 1933.[25] While there are different means of becoming an accredited investor, the basic qualification is possession of at least $5 million in investments.[26] Of course, an average retail investor will not have $5 million, let alone $5 million tied up in investments. This means that hedge fund investing is off limits to most of America, including the millions of people who fall under the SEC’s definition of retail investor.

Rise of Technology Conducive to Retail Investing

It goes without saying that as technology has grown and developed, the general capabilities of average Americans have grown and developed with it. This is true for the investing world also, where average citizens can easily utilize online platforms and applications on their phones to invest money in the market.[27] This section provides a brief discussion of the implications of online investing, as well as the relatively recent development of fee-free investing, which has been key to the recent monumental growth in retail investing.[28]

Online Brokerages

The 1990s marked the rise of the online brokerage firm. In 1995, E*Trade “became the first online brokerage firm,” deriving more than 80% of its revenues from trading commissions.[29] E*Trade was founded to provide online brokerage services to other brokers such as Charles Schwab and Fidelity.[30] Just a few years into its existence, however, the firm decided on a direct-to-consumer strategy, cutting out the middleman and appealing straight to investors looking to take advantage of the speed that an online brokerage has to offer.[31] Soon after E*Trade entered the online brokerage market other companies followed, bringing in the age of the online brokerage.[32]

Retail traders lauded the combination of improved access to data and information, as well as the cost decrease in processing trades and the general ease of trading securities online.[33] By 1995, over 20 percent of America’s population invested in stock at some level; just 10 years previous, that number was 5 percent.[34] Now, the vast majority of stock trading occurs on online brokerage sites, and the number of users grows daily. [35] According to a Gallup poll taken in March and April 2020, 55% of Americans report owning stock.[36] This includes direct ownership of stock through a brokerage account, as well as stocks owned through retirement savings accounts and mutual funds.[37]

The 21st century heralded rapid expansion in this technology, and the United States went from having 12 online brokerage firms in 1994 to 140 firms by 2001.[38] The increase in competition meant the creating of platforms that were more user-friendly, as well as faster trading, lower fees, and never-before-seen features.[39] As well as this, there was the dawn of the day trader; a day trader being someone who commits entirely to online trading as a full-time job. Day trading became possible throughout the 1990s and it has continued to grow in popularity ever since.[40] Notably, as a survey of securities and trading law makes clear, the legislature has been slow to adapt to the changes in trading that increasing technological advancement has wrought.[41]

Fee-Free Investing

In 2014, Robinhood launched the first commission-free trading platform.[42] This was a huge step forward in the retail investment world, where before Robinhood it was necessary for traders to pay $5-7 per trade and have a minimum of $500 to start with.[43] Other brokerages soon followed with this same strategy, and now fee-free trading with no initial minimums is the new normal.[44] One cannot overstate how this change to fee-free trading across all major platforms, coupled with the Coronavirus pandemic which left millions of people bored at home and receiving stimulus checks, led to the incredible rise in retail investment.[45] Technology has truly been the great equalizer in this area with people now having easy access to the markets like never before.

How Technology Allows for Sophisticated Retail Action

Individual investors now have access to an enormous and unprecedented amount of financial information at their fingertips. Technology has allowed for the standardization of formats and makes it easier for investors to repurpose information from across platforms to produce more accurate data.[47] Education (coupled with access to platforms and technology) now allows retail investors to be a serious force in the markets and has led to recent questions of how to possibly regulate and curtail this force, through law and oversight.

Even back in 1997, the SEC recognized the dramatic shift that was occurring in the investment world, with retail investors growing in knowledge and sophistication because of the increasing role of technology:

Twenty years ago, many individual investors did not actively manage their investments . . . . An individual investor in today’s society, however, is far more likely to consider actively his or her financial circumstances and possible investment options. The vast amount of information accessible to retail investors, and the various tools available to enable such investors to sort, search and save data quickly, have dramatically altered the profile of the “typical” . . . investor. . . .”[48]

In the SEC’s view, if an investor had a computer and an internet modem then they could receive all the data necessary to make informed trades.[49] Data such as prospectuses, commentary, and investment advice could all be had same day, without ever leaving the house.[50] In fact, the SEC recognized that advancements in technology were encouraging people to make the home computer the primary tool for researching and tracking their portfolios. The report continues:

As a result of this revolution in information availability, many investors believe they no longer need the assistance of a broker or other professional to do their financial planning for them. The Commission has recognized that millions of [investors] are taking a more active approach to their investments . . . . As the Commission and the securities industry continue to accommodate the needs of this new retail investor, the power of electronic media likely will grow.[51]

More than twenty years have passed since the SEC reported this information to Congress and, given the information relayed so far in this Article, the predictions have proved prescient.

GameStop: A Case Study

On October 15, 2020, Global X, a leader in the retail investment world, said the following about the current state of the market:

We believe COVID-induced unemployment and boredom combined with opportunity and access jumpstarted the renewed rise of the retail investor. Nationwide economic shutdowns resulted in 30.8 million initial jobless claims in March and April. Months on end in the same space with limited social interaction can get boring, especially after exhausting the Netflix queue. With lockdowns shutting down most professional sports and the gambling that accompanies them, many people were left craving excitement and stimulus. In this environment, many gamblers shifted from sports to stocks looking for quick gains and cheap thrills.[52]

Global X has not been the only one to make such claims. Indeed, its claims are backed up by recent research. Deutsche Bank recently conducted a survey where 430 online investors were asked how they planned to use their stimulus checks.[53] Half of the respondents aged 25 to 34 years old said that they planned to spend 50% of their stimulus payments on stocks; all of the 18 to 24-year-old retail investors involved in the survey planned to use up to 40% of any stimulus checks on stocks; and all of the 35 to 54-year-old retail investors surveyed planned to use up to 37% of their checks on stock market investment.[54]

The implication is that young people receiving large sums of money and using commission-free investment vehicles are continuing to make up the bulk of the total number of investors.[55] This can be seen no better than in the case of GameStop, which offers an ongoing example of the tension between the burgeoning retail investor sphere and the old guard of institutional hedge funds. The GameStop stock saga is still making headlines, with the key players recently appearing before the House Financial Services Committee, on February 18, 2021.[56]

After retail investors caused GameStop’s stock price to increase over 1600% in just a couple of weeks, many people wondered whether retail investors are somehow responsible for market manipulation.[57] Certainly, the situation has brought awareness to the new realities of the investing world. With technology, the average citizen is now able to find and compile key information faster and more efficiently than ever.[58] Additionally, online forums such as Reddit’s WallStreetBets allow otherwise disparate individual investors to communicate and act in unison in a way never been seen on Wall Street.[59]

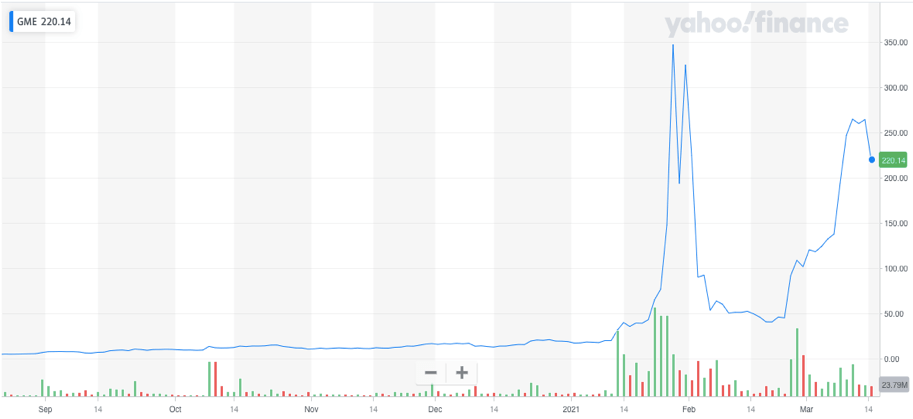

On Wallstreet, retail investors are often referred to as “dumb money.”[60] They are seen as perpetual losers to the institutional investment machine, with its traders and analysts who invest money for a living.[61] However, on social forums like Reddit’s WallStreetBets, these individual investors can communicate together and tackle a single stock in large numbers.[62] In the case of GameStop, these retail investors banded together to take on hedge funds that were betting that GameStop stock would fall, shorting the stock in anticipation of this fall in an effort to make money off of it: “While the hedge funds and other professional money managers had been shorting GameStop’s shares, betting that its stock was doomed to further decline, the retail investors — online traders, mom-and-pop investors, small brokers and others — have been pushing the other way, buying shares and stock options.”[63] This value increase can easily be appreciated in the below graph; and, while GameStop is not the only stock to receive such treatment, it is the most notable. This is largely because it has caught the attention of the federal government and has been the impetus for a call by some for more regulation of such retail investment activity.[64]

Congress

On February 18, 2021, the House Financial Services, in an effort to understand what exactly happened during the GameStop frenzy, conducted a hearing involving the catalyst behind Reddit’s GameStop frenzy (Keith Gill), along with Reddit CEO Steve Huffman, Robinhood CEO Vlad Tenev, and Kenneth C. Griffin and Gabriel Plotkin, CEOs of Citadel and Melvin Capital, respectively, two hedge funds who had shorted GameStop’s stock.[66] Robinhood was the focus of the hearing, since the Robinhood application in large part facilitated the retail investor GameStop purchase frenzy until Robinhood could no longer handle the volume of trades.[67]

When the trading was at its peak, Robinhood disallowed the purchase of GameStop stock.[68] This prompted some lawmakers to call for the House Financial Services hearing to investigate Robinhood’s relationships with institutional investors (like the hedge funds which shorted GameStop stock).[69] At the hearing, Robinhood’s CEO stated that there was no collusive relationship between the company and institutional investors.[70] Tenev told those at the hearing that the company had to stop all purchases of GameStop for a time because its business partners, the clearinghouses that perform the trades, increased the amount of money Robinhood would have to pay if it wanted those trades cleared.[71]

This hearing highlighted the need for securities law to catch up with present-day technology and recognize the new dynamic that exists between institutional and retail investors. Whereas before it was perhaps unnecessary to consider the interplay of these two district investing worlds, the legislature must promulgate new laws which acknowledge this reality. For instance, as became clear in the hearings, hedge funds are employing certain tactics meant to hinder the work of large groups of retail investors working towards a common goal.[72] Such tactics, like short-ladder attacks meant to lower the price of a stock, were likely not so prevalent before retail could coordinate. But these tactics are akin to market manipulation, and the law must recognize that market manipulation will in all likelihood become more common among institutions as they increasingly find themselves at odds with monoliths of retail investing.

Implications for the Future

Without a doubt, the shape of the United States financial market is changing, and certainly will not be the same as it was just a few years ago. Technology has created great opportunities for people to make money in the markets. Brokerages like E*TRADE and Robinhood have helped democratize the market, revolutionizing the landscape such that fee-free trading and easy sign-up are now the norms instead of the outliers. Retail investors can now buy and sell stocks and learn about companies instantaneously. Anyone with a smartphone or a computer can sign-up and place a trade; and social media allows for unprecedented communication and information sharing, to the extent that a social forum can drastically impact the market. With this, there are also questions raised about the legal ramifications of apparent market collusion. Surely, though, technology has only worked to level the playing field. Retail investors are now in a position to make their presence known in the markets and benefit from a system that remains stacked against them. One would think the legal landscape should reflect this new reality, and work to protect retail instead of working to break it up and return it to its status of old. This Article supports the continuing change and believes we should recognize and laud the great boon that technology is in this area, as well as advocate for a system of laws that doesn’t attempt to wind back the clock to darker times.

In surveying the field of securities trading law for the writing of this Article, one thing is clear: the law is behind, and many people are ignorant. The law is behind in terms of controlling certain activities of institutional investors that arise solely because of the increased coordination between retail investors. Hedge funds should not be allowed to manipulate the market just because retail is capable of investing in a coordinated fashion that may run counter to institutional goals. As well as this, any calls for heightened regulation of retail in order to avoid coordinated stock purchases should be answered, not with regulation, but with education. Simply because individual retail investors now have the capacity to gain in-depth market knowledge, and communicate this knowledge amongst themselves, does not mean that retail is manipulating the market. What it means is that, with technology, the playing field is as level as it has ever been. Laws should not be enacted which work only to reinstitute disparities that technology has worked to eradicate.

[1] Robert Gebeloff, Who Owns Stocks? Explaining the Rise in Inequality During the Pandemic, N.Y. Times (Jan. 26 2021), available athttps://www.nytimes.com/2021/01/26/upshot/stocks-pandemic-inequality.html.

[2] Shuonan Chen, The Information Gap between Institutional and Retail Investors during the IPO Process, in The Political Economy of Financial Regulation, 63–101, (Emilios Avgouleas & David C. Donald eds., 2019).

[3] Laurie Havelock, Ten steps for building a retail investor strategy, IR Magazine (Mar. 26, 2015), available athttps://www.irmagazine.com/shareholder-targeting-id/ten-steps-building-retail-investor-strategy.

[4] James Royal, Best online stock brokers for beginners in March 2021, Bankrate (Mar. 1, 2021), https://www.bankrate.com/investing/best-online-brokers-for-beginners/.

[5] Noelle Acheson, Who Has the Power, Retail or Institutional Investors?, Coindesk (June 1, 2019), available at https://www.coindesk.com/who-has-the-power-retail-or-institutional-investors.

[6] Tomi Kilgore, GameStop stock rallies, after soaring more than 550% amid a 3-week win streak through Friday (visited Mar. 15, 2021), available at https://www.marketwatch.com/story/gamestop-stock-rallies-after-soaring-more-than-550-amid-a-3-week-win-streak-through-friday-2021-03-15.

[7] Nikhilesh De, State of Crypto: How Will the Government React to GameStop? (Feb. 3, 2021), available at https://www.coindesk.com/gamestop-regulators-response.

[8] Nasdaq, Retail Investors, nasdaq.com, https://www.nasdaq.com/glossary/r/retail-investors (last visited Mar. 15, 2021).

[9] Michael Kalscheur, Individual Stocks vs. Mutual Funds, Castle Wealth Advisors (Feb. 2010), available at https://www.castle3.com/next-generation-articles/129-individual-stocks-vs-mutual-funds.

[10] Federal Reserve, Balance Sheet of Households and Nonprofit Organizations, 1952 – 2020, federalreserve.gov, https://www.federalreserve.gov/releases/z1/dataviz/z1/balance_sheet/chart/#series:financial-assets;units:shares (last visited Mar. 29, 2021).

[11] TD Ameritrade, About TD Ameritrade, tdameritrade.com, https://www.tdameritrade.com/about-us.page#:~:text=Today%2C%20TD%20Ameritrade%20provides%20investing,6%2C000%20independent%20registered%20investment%20advisors (last visited Mar. 29, 2021).

[12] David Curry, Robinhood Revenue and Usage Statistics (2021), Business of Apps (Mar. 8, 2021), available athttps://www.businessofapps.com/data/robinhood-statistics/.

[13] Id.

[14] Fidelity, By the Numbers, fidelity.com, available at https://www.fidelity.com/about-fidelity/our-company#:~:text=Who%20we%20serve,solutions%20to%20grow%20their%20businesses.

[15] Vanguard, Fast facts about Vanguard, https://about.vanguard.com/who-we-are/fast-facts/ (last visited Mar. 29, 2021).

[16] Kevin Voigt, 11 Best Online Brokers for Stock Trading of April 2021, Nerdwallet (Mar. 22, 2021), https://www.nerdwallet.com/best/investing/online-brokers-for-stock-trading.

[17] Nasdaq, Institutional Investors, nasdaq.com, available at https://www.nasdaq.com/glossary/i/institutional-investors (last visited Mar. 29, 2021).

[18] Id.

[19] Kimberly Amadeo, Hedge Fund Investors: Who They Are and Why They Do It, The Balance (Jan. 23, 2021), available athttps://www.thebalance.com/who-invests-in-hedge-funds-and-why-3306239.

[20] United States Securities and Exchange Commission, Mutual Fund, sec.gov, https://www.sec.gov/investor/tools/mfcc/mutual-fund-help.htm (last visited Mar. 29, 2021).

[21] SEC Office of Investor Education and Advocacy, Investor Bulletin: Hedge Funds, sec.gov, available athttps://www.sec.gov/files/ib_hedgefunds.pdf (last visited Mar. 29, 2021).

[22] Id.

[23] Id.

[24] Id.

[25] 17 CFR § 230.501(a).

[26] Jessica Forbes, et. al., SEC Expands Definition of “Accredited Investor”, Harvard Law School Forum on Corporate Governance (Apr. 12, 2021), available at https://corpgov.law.harvard.edu/2020/09/18/sec-expands-definition-of-accredited-investor/.

[27] Eric Rosenberg, Best Stock Trading Apps of 2021, The Balance (Feb. 17, 2020), available at https://www.thebalance.com/best-stock-trading-apps-4159415.

[28] Tim Fernholz, How no-fee stock trading is changing the stock market, qz.com (Sept. 22, 2020), available at https://qz.com/1906670/how-robinhoods-no-fee-stock-trading-is-changing-the-stock-market/.

[29] Jennifer Wu, Michael Siegel and Joshua Manion, Online Trading: An Internet Revolution, Research Note: Sloan School of Management Massachusetts Institute of Technology (June, 1999), available at http://web.mit.edu/smadnick/www/wp2/2000-02-SWP%234104.pdf.

[30] Id.

[31] Id.

[32] Id.

[33] Id.

[34] Stock-Trading-Warrior, The Meteoric History of Online Stock Trading, stock-trading-warrior.com, http://www.stock-trading-warrior.com/History-of-Online-Stock-Trading.html (last visited Mar. 15, 2021).

[35] Matt Miller, The Best Online Brokers for 2021: The Rise of the Individual Investor and Fintech Apps, Barron’s (Feb. 27, 2021), available athttps://www.barrons.com/articles/the-best-online-brokers-for-2021-the-rise-of-the-individual-investor-and-fintech-apps-51614378865.

[36] Lydia Saad, What Percentage of Americans Owns Stock, Gallup.com (June 4, 2020), available athttps://news.gallup.com/poll/266807/percentage-americans-owns-stock.aspx.

[37] Id.

[38] BEBUSINESSED, History of Online Stock Trading, bebusinessed.com, https://bebusinessed.com/history/history-of-online-stock-trading/ (last visited Mar. 15, 2021).

[39] Id.

[40] Id.

[41] Troy Paredes, Innovation and Securities Regulation, The Regulatory Review (Oct. 6, 2020), available athttps://www.theregreview.org/2020/10/06/paredes-innovation-securities-regulation/.

[42] Josh Constantine, Robinhood Launches Zero-Fee Stock Trading App, techcrunch.com (Dec. 11, 2014), https://techcrunch.com/2014/12/11/robinhood-free-stock-trading/.

[43] Jason Wenk, The real story behind commission free trading, grow.altruist.com (Oct. 16, 2019), https://grow.altruist.com/the-real-story-behind-commission-free-trading.

[44] Daisy Maxey, ‘Free’ Trading Has Arrived. Be Sure to Read the Fine Print, Barron’s (Oct. 8, 2019), https://www.barrons.com/articles/free-trading-has-arrived-be-sure-to-read-the-fine-print-51570208401.

[45] Angelita Williams and Eric Young, New Research: Global Pandemic Brings Surge of New and Experienced Retail Investors Into the Stock Market, finra.org (Feb. 2, 2021), https://www.finra.org/media-center/newsreleases/2021/new-research-global-pandemic-brings-surge-new-and-experienced-retail.

[46] Sarim Mehmood, How Retail Investors Took Over The Stock Market, Block Publisher (June 11, 2020), https://blockpublisher.com/how-retail-investors-took-over-the-stock-market/.

[47] Kevin McAllister, How will technology influence the role of the individual investor most in the next five years?, protocol.com (Feb. 19, 2021), available at https://www.protocol.com/fintech/how-tech-reshapes-retail-investing?rebelltitem=6#rebelltitem6.

[48] U.S. Securities and Exchange Commission, Report to the Congress: The Impact of Recent Technological Advances on the Securities Markets, sec.gov (Nov. 26, 1997), available at https://www.sec.gov/news/studies/techrp97.htm.

[49] Id.

[50] Id.

[51] Id.

[52] Frank Van Dyke, The Renewed Rise of the Retail Investor, Global X (Oct. 15, 2020), available at https://www.globalxetfs.com/cio-corner/the-renewed-rise-of-the-retail-investor/.

[53] Holly Ellyat, Young retail investors plan to spend almost half of their stimulus checks on stocks, Deutsche survey claims, msn.com (Mar. 8, 2021), available at https://www.msn.com/en-us/money/markets/young-people-looking-to-spend-almost-half-of-their-stimulus-checks-on-stocks-deutsche-survey-finds/ar-BB1emAUd.

[54] Id.

[55] Id.

[56] Tory Newmyer, Douglas MacMillan & Hamza Shaban, Congress presses Robinhood CEO on company’s role in GameStop stock frenzy, washintonpost.com (Feb. 18, 2021), available at https://www.washingtonpost.com/business/2021/02/18/gamestop-robinhood-citadel-roaring-kitty-hearing-live-updates/.

[57] Reuters Staff, Timeline: GameStop’s 1,600% surge in retail investor vs hedge fund battle, reuters.com (Jan. 27, 2021), available athttps://www.reuters.com/article/us-gamestop-hot-timeline/timeline-gamestops-1600-surge-in-retail-investor-vs-hedge-fund-battle-idUSKBN29W237.

[58] Farm Bureau Financial Services, 4 Ways Technology Has Changed Investing, fbfs.com (Feb. 6, 2020), available athttps://www.fbfs.com/learning-center/4-ways-technology-has-changed-investing.

[59] Wayne Duggan, GameStop’s Power Surge: Will WallStreetBets Or The Short Sellers Come Out On Top?, aol.com (Jan. 22, 20201), available athttps://www.aol.com/news/gamestops-power-surge-wallstreetbets-short-204539709.html.

[60] Matt Phillips and Taylor Lorenz, ‘Dumb Money’ Is on GameStop, and It’s Beating Wall Street at Its Own Game, nytimes.com (Jan. 27, 2021), available at https://www.nytimes.com/2021/01/27/business/gamestop-wall-street-bets.html.

[61] Id.

[62] Shona Ghosh, Reddit group WallStreetBets hits 6 million users overnight after a wild week of trading antics, Business Insider (Jan. 29, 2021), available at https://www.businessinsider.com/wallstreetbets-fastest-growing-subreddit-hits-58-million-users-2021-1.

[63] Id.

[64] Ben Winck, The Reddit-fueled GameStop rally is reportedly under federal investigation for possible market manipulation – and Robinhood has been subpoenaed, Markets Insider (Feb. 11, 2021), available at https://markets.businessinsider.com/news/stocks/reddit-gamestop-stock-rally-investigation-market-manipulation-robinhood-regulation-gme-2021-2-1030074397.

[65] Yahoo! Finance, GameStop Corp. (GME) NYSE – NYSE Delayed Price. Currency in USD, finance.yahoo.com,

https://finance.yahoo.com/quote/GME/chart (last visited Mar. 15, 2021).

[66] Makena Kelly, Hill Report: who wants to talk to Reddit?, The Verge (Feb. 18, 2021), available athttps://www.theverge.com/2021/2/18/22290110/house-financial-services-robinhood-gamestop-squeeze-roaringkitty-hearing.

[67] Id.

[68] Id.

[69] Id.

[70] Id.

[71] Id.

[72] Id.

Leave a comment